International Equities: A Clearer, More Consistent Framework – March 2026

Traditional asset‑allocation models typically recommend allocating a portion of an equity portfolio to international stocks. The rationale is straightforward: investing outside an investor’s home market counters home‑country bias and provides access to companies, industries, and earnings streams that behave differently than domestic exposures. International diversification can include both developed and emerging markets.

However, focusing solely on a company’s country of domicile is no longer sufficient to capture true global diversification. Several structural shifts in the global economy and in corporate behavior challenge the traditional model:

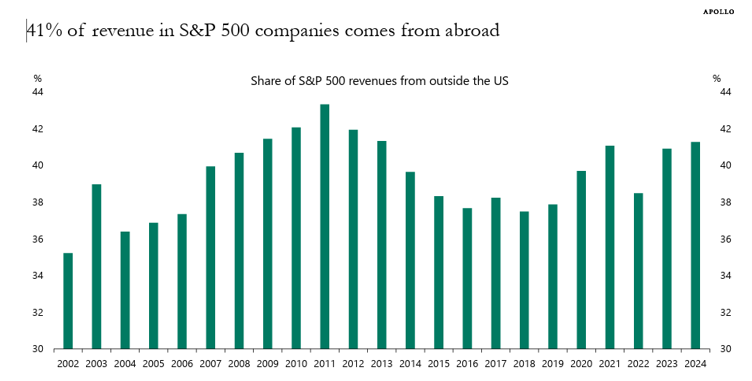

• **U.S. multinationals are already global operators.** Many S&P 500 companies generate substantial portions of their revenue overseas—41% in 2024, according to Apollo Global. While headquartered in the U.S., these companies operate across all major regions with earnings translated and hedged back into U.S. dollars.

• **U.S. firms often maintain superior profitability.** In many industries, U.S. companies have higher margins and stronger earnings growth than their international peers.

• **Foreign-domiciled companies face different operating environments.** Legal, political, and governance frameworks differ significantly across markets and have resulted in several high‑profile issues in environmental, financial, and ethical areas.

Source: FactSet, Apollo Chief Economist

At the same time, global investing requires a dynamic—not static—approach. Shifts in tax, trade, and immigration policy by the United States have led countries around the world to introduce their own fiscal and industrial‑policy adjustments. As a result, country-level considerations are becoming more relevant again. While we do not view domicile alone as a complete measure of diversification, today’s geopolitical and economic environment makes it more important than it has been in many years.

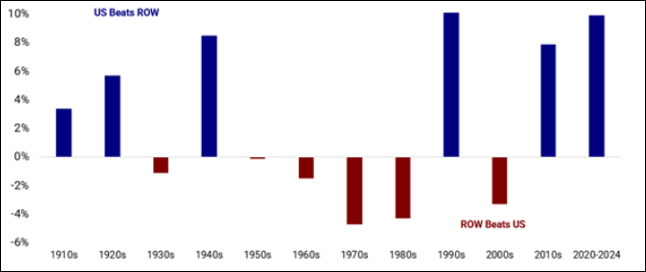

Another powerful long-term consideration is **reversion to the mean**. Historically, leadership between U.S. and international markets has alternated across cycles. For most of the period since 1990, U.S. equities have outperformed significantly. This trend extended through the 2010s and early 2020s, supported by superior fundamentals and a strong U.S. dollar. However, 2025 marked a reversal: international equities outperformed U.S. markets as the dollar weakened.

Source: UBS, DMS Database, 2024, Breakout Capital Calculations. Note: Expressed in real USD terms

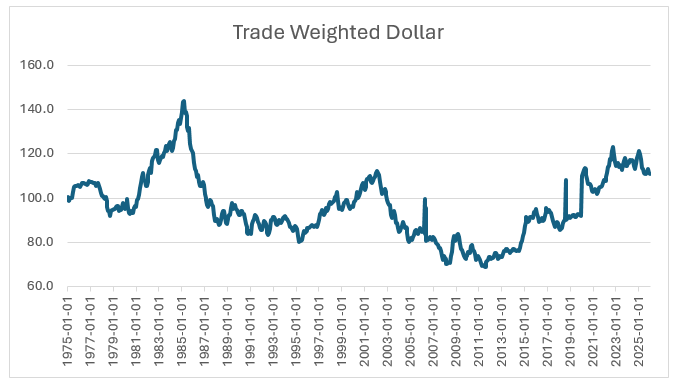

A sustained decline in the dollar has historically coincided with stronger performance from international markets. Should recent currency trends continue, the relative attractiveness of non‑U.S. equities could further improve.

Source: Federal Reserve Economic Data, Federal Reserve Bank of St. Louis

In addition to currency effects, investors evaluating international allocations may consider:

• **Valuations:** International equities often trade at a discount to U.S. markets. While lower valuation alone is not sufficient, it may enhance future expected returns if growth and quality dynamics stabilize or improve.

• **Volatility:** International markets can deliver differentiated volatility patterns that may improve overall portfolio risk characteristics.

• **Dividend yields:** Many international markets—particularly in Europe and parts of Asia—offer higher dividend yields than the U.S.

Structural reforms are also underway across various regions. Several Asian economies are strengthening corporate governance standards, while European markets continue to integrate economically and financially. These changes may support long‑term investment flows.

Finally, economic fundamentals may increasingly favor international markets. The International Monetary Fund projects that more than 80% of major emerging economies will grow faster than the United States over the next five years—potentially shifting investor sentiment toward non‑U.S. opportunities.

Taken together, these trends suggest that while U.S. equities remain global leaders, investors may benefit from a more balanced approach to international diversification—one that incorporates fundamentals, currency dynamics, and structural economic shifts rather than relying solely on domicile.

Firm Definition and Contact Information

Maple Capital Management, Inc. (MCM) is an independent SEC Registered Investment Advisor with offices in Montpelier, Vermont and Atlanta, Georgia.

This commentary reflects the views of MCM and should not be considered to be investment or financial advice. MCM does not warranty these views and will not update this communication after the date of publication. Any mention of specific securities is done for illustrative purposes and the securities mentioned may or may not be held in client accounts. No assumption or assurance should be taken that securities mentioned will be safe or profitable investments. Past performance is not indicative of future results

For further information, please contact David Bosworth at 1-802-229-2838 or at [email protected]. For further information about Maple Capital, including a copy of our informational brochure, please visit our website at www.maplecapital.com.

Disclaimer

This document is a general communication being provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature or other purpose in any jurisdiction. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and determine, together with their own financial professional, if any investment mentioned herein is believed to be appropriate to their financial situation and investment profile. Investors should ensure that they obtain all available relevant information before making any investment. It should be noted that investments involve risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yields are not reliable indicators of current and future results. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted.

Past performance does not guarantee future results. Diversification does not guarantee investment returns and does not eliminate the risk of loss.

The post International Equities: A Clearer, More Consistent Framework – March 2026 appeared first on Maple Capital Management.