Assessing the Lasting Economic Effects of the Iran War – May 2026

The outbreak of war in Iran has introduced a classic geopolitical shock to the global economy, defined by sharp increases in energy prices, heightened uncertainty, and near-term volatility across financial markets. As investors look beyond the immediate disruption, the central question is whether these effects will persist after any potential peace settlement is reached or ultimately fade as a transitory shock.

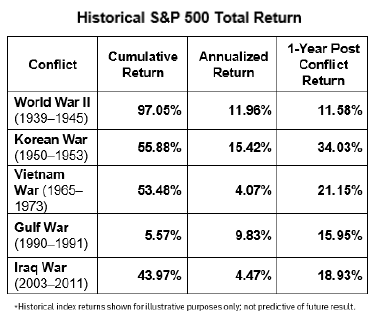

History offers a useful starting point. Geopolitical events, while often severe in the short run, have typically had limited lasting impact on global equity markets. Over the past several decades, markets have tended to recover and even post gains following such shocks as economic activity normalizes and uncertainty recedes. This suggests that, in isolation, any war itself is unlikely to permanently derail broader economic growth or long-term market returns.

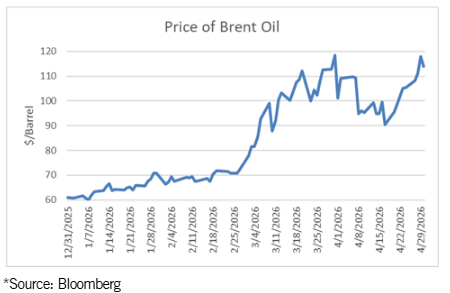

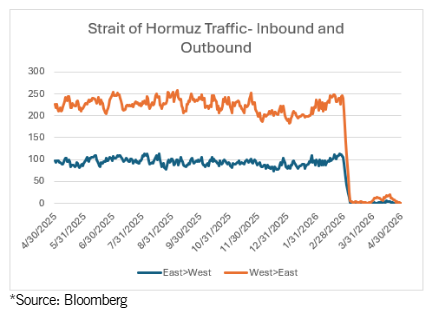

That said, one of the key impacts from this conflict is clear and meaningful: energy. The disruption of supply routes, most notably through the Strait of Hormuz, which handles a significant share of global oil flows, has driven crude prices sharply higher and contributed to inflationary pressures worldwide. Even if hostilities cease, the aftereffects may linger. Energy infrastructure damage, estimated in the tens of billions of dollars1 will take time to repair and will likely prolong tightness in global markets.

In the near to intermediate term, this implies that inflation may remain elevated even after a potential peace agreement. Higher fuel and input costs ripple through transportation, manufacturing, and food production, placing pressure on consumers, corporations, and governments that need to grapple with the impact. These dynamics could delay central bank easing cycles and keep interest rates higher for longer, an outcome with clear implications for both equities and fixed income.

However, the persistence of these effects depends heavily on duration and structural changes that

follow. If the war proves relatively short-lived and supply chains normalize quickly, much of the economic damage is likely to reverse. Commodity prices would likely stabilize, inflation should moderate, and pent up demand could support a cyclical rebound. In this scenario, the war would resemble prior geopolitical shocks: disruptive, but ultimately temporary.

The more lasting impact may instead emerge through second-order effects. The conflict reinforces the fragility of global energy systems and may accelerate investment in energy diversification, including domestic production and renewables. It also contributes to a broader shift toward geopolitical fragmentation, where supply chains are reconfigured for resilience rather than efficiency. In addition, increased defense spending, already a feature of this conflict, could place sustained upward pressure on fiscal deficits and long-term interest rates.

From an investment perspective, the conclusion is nuanced. The direct economic effects of the Iran war are unlikely to be permanently impairing for global markets, particularly if a credible peace settlement is reached.

However, the conflict may leave a lasting imprint on inflation dynamics, fiscal policy, and geopolitical risk premiums. In other words, while the shock may fade, the environment it reinforces, characterized by higher volatility and structurally higher geopolitical risk, could persist.

For investors, this argues less for wholesale portfolio changes and more for thoughtful positioning. Maintaining diversification, recognizing the potential for continued macro volatility, and selectively allocating to areas that benefit from any structural shifts remain key. As always, Maple Capital stands ready to help guide you through these uncertain times.

- 1. Reuters, Rystad Energy

Firm Definition and Contact Information

Maple Capital Management, Inc. (MCM) is an independent SEC Registered Investment Advisor with offices in Montpelier, Vermont and Atlanta, Georgia. This commentary reflects the views of MCM and should not be considered to be investment or financial advice. MCM does not warranty these views and will not update this communication after the date of publication. Any mention of specific securities is done for illustrative purposes and the securities mentioned may or may not be held in client accounts. No assumption or assurance should be taken that securities mentioned will be safe or profitable investments. Past performance is not indicative of future results.

For further information, please contact David Bosworth at 1-802-229-2838 or at [email protected]. For further information about Maple Capital, including a copy of our informational brochure, please visit our website at www.maplecapital.com.

Disclaimer

This document is a general communication being provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature or other purpose in any jurisdiction. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and determine, together with their own financial professional, if any investment mentioned herein is believed to be appropriate to their financial situation and investment profile. Investors should ensure that they obtain all available relevant information before making any investment. It should be noted that investments involve risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Both past performance and yields are not reliable indicators of current and future results. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted.

Past performance does not guarantee future results. Diversification does not guarantee investment returns and does not eliminate the risk of loss.

www.maplecapital.com | 535 Stone Cutters Way, Montpelier, VT 05602 | Toll Free: 800.255.9946

The post Assessing the Lasting Economic Effects of the Iran War – May 2026 appeared first on Maple Capital Management.